Today is May Day and the ACA is still alive. Donald Trump’s campaign boast that he would sign a bill repealing the Affordable Care Act (ACA/ObamaCare) on his inauguration day is long gone and forgotten. House Speaker Paul Ryan and Senate Majority Leader Mitch McConnell’s gamble that by April 28th the ACA would be effectively decimated using the expedited budget reconciliation process proved to be a sucker’s bet.

Undeterred, White House and House operatives are trying by Wednesday to line up 216 votes—not to pass the Republicans’ American Health Care Act (AHCA) but to feign signs of progress to dampen the white-hot anger of the Republican base at their Party leaders’ inability to enact the ACA repeal promised since the law’s signing on March 23, 2010. They want to take a third run at it this week and perhaps succeed after two prior failures. Senate Republicans, meanwhile, are crossing their fingers hoping that the House fails, sparing the upper chamber the funerary duties. For the Senate to advance ACA repeal now, a new and wholly unimagined bill would need to be constructed.

The level of legislative malpractice evidenced by Speaker Ryan and his team since January is staggering and perplexing. They designed a bill that the Congressional Budget Office estimated would cause 24 million Americans to lose health insurance. They advanced a proposal that provoked public opposition from the American Hospital Association, the American Medical Association, the American Nurses Association, AARP, and hundreds of other national organizations representing Americans with serious stakes in our health care system. They invented a plan that generated unprecedented grassroots support for the ACA and fierce opposition aimed at them. For the first time, Ryan’s plan turned most Americans into ACA supporters. His legislation generated support from only 17% of Americans, an unheard of level of non-support.

Why did they do this and why do they persist?

Trump and Ryan both showed their hands in recent public statements linking ACA repeal with their tax cut agenda; Trump’s tax plan was released in one-page outline form this past week. To Republicans, the ACA’s poison is not the insurance expansion that bears remarkable resemblance to the two public health insurance programs they have always loved: Medicare Part C or Medicare Advantage, and Medicare Part D, the outpatient prescription drug benefit. Continue reading “MayDay! The ACA Is Still Alive and Still in Danger”

GLOBAL HEALTH EXPERT Michael Reich says that the acid test of any national health reform comes when a new national administration takes over. Only when a new president or prime minister assumes power can we judge the stability and staying power of any health system reform. In the US, that’s this moment. Since November 8, we’ve been learning what parts of the Affordable Care Act (ACA) have staying power, which do not, and what’s uncertain.

Right now, after Friday’s demise of the Republican repeal and replace plan, the American Health Care Act (AHCA), we know that Medicare, Medicaid, insurance market reforms such as guaranteed issue, and delivery system reforms such as accountable care organizations look

safe. We know that the private insurance coverage reforms – insurance exchanges, premium and cost-sharing subsidies, the individual mandate – are at risk and in danger even though they dodged full repeal with the AHCA’s demise. And we don’t know the fate of the ACA’s many tax increases. Let’s view these systematically. Continue reading “The State of Play Post-Trump/RyanCare”

THE BIG NEWS IS, of course, Monday’s “score” from the Congressional Budget Office detailing that the House Republican bill to repeal and replace the Affordable Care Act/Obamacare will result in 14 million Americans losing health insurance by 2018 and 24 million by 2026.

Before that, something else caught my eye from the Bangor Daily News. It’s a blog post from a woman named Crystal Sands who writes about how the ACA enabled her and her young family to take a chance and find a new life as farmers. Her post, “The ACA makes a simpler farming life possible for our family,” says this:

“I’m a writer, an online professor, a farmer, a wife, and a mom. None of these jobs offer health insurance for me and my family, so our family purchases our health insurance through the Affordable Care Act. We work hard, but we try to work differently. If you read my blog, you know we’re learning to grow and raise our own food, and our health insurance through the ACA makes this possible. …

“The ACA has helped me to become a better mom, a better wife, a better teacher because I am not so overworked, and it has made it so I can learn to be a farmer. I’m also just a better person. I’m not sick and overworked. I’m more patient and more kind and more helpful to everyone.And this is my story. There’s so much potential here to make lives better. There are many people, including many farmers, who depend on the ACA. I hope we don’t lose sight of that.”

SO, REPUBLICANS ARE planning a major blitz to repeal and delay/replace/collapse the Affordable Care Act/ACA/ObamaCare. I’ve got five questions to ask leaders of the Grand Old Party.

First, if your guarantees are honest that your replacement law will be better than the ACA, why not share real numbers?

Your message is “trust us.” Would businessman Trump take such a deal?

Second, when you promise to continue “guaranteed issue” of health insurance with no-pre-existing conditions or medical underwriting, why do you always fail to mention the fine print?

Trump, Ryan, and other Republicans’ statements are clear – any reform will maintain “guaranteed issue.” Yet your written plans tell another story – guaranteed issue will be kept only for persons who maintain “continuous coverage” (undefined). This means if you lose your insurance and have a coverage gap beyond the allowed time, you will be newly subject to medical underwriting and pre-existing condition exclusions for an unspecified period (forever?).

How many people might fall into this new medical underwriting Circle of Hell (CoH)? Start with 28-29 million currently uninsured, add the estimated 20-30 million increase because of Republican plans to eliminate income-based premium subsidies. We start at 48-58 million Americans, and the numbers will only grow as more fall into the medical underwriting CoH.

This is detailed in numerous replacement plans, including Ryan’s. Yet you never mention this life-important detail when talking with media who buy your line that you will continue the ACA’s elimination of pre-existing conditions for everyone. Untrue.

Third, what will you do about enormous losses for those dealing with substance abuse and mental health needs under your plans?

Most Americans don’t realize that the ACA is the biggest law ever in covering Americans for substance abuse and mental health services (aka: behavioral health). It’s true. ACA guaranteed issue means no one can be denied insurance because they had or have substance abuse/mental health problems. Bans on lifetime and annual benefit limits allows countless persons with expensive substance abuse or mental health disorders to keep covered. Requiring insurers to cover 10 “essential health benefits” insures that nearly all Americans have behavioral health coverage (#5) PLUS prescription drugs (#6) to treat their disorders.

All Republican plans – Trump, Ryan, Price etc. – propose eliminating “essential health benefits.” They propose eroding guaranteed issue (see above) and canceling elimination of annual benefit limits. So, the ACA’s enormous advances for mental health and substance abuse would become major losses under Republicans’ plans. I’m not sure you get this at all. I am certain most Americans have zero idea of this and they will strongly object when they find out.

Fourth, why are you so mean to the nation’s hospitals?

In crafting the ACA, America’s hospitals committed a mortal sin in Republicans’ eyes by making a deal with President Barack Obama and the US Senate. In exchange for Democrats’ commitment to get as close to universal coverage as politically possible, hospitals agreed to $155 billion in federal payment reductions between 2010-19 (now about $350 billion between 2016-2025). They did this to stop being the default caretakers of America’s uninsured.

Now Republicans plan to repeal the ACA’s new taxes on wealthy Americans, on drug, medical device, and health insurance companies, even on indoor tanning salons! And, they plan to leave in place the $350 billion in payment cuts to hospitals even as their policies will send as many as 30 million recently insured Americans back into the ranks of the uninsured and back to America’s emergency departments.

The American Hospital Association and the Federation of American Hospitals, who brokered the 2009 deal, wrote a letter on December 7 to Republicans: “…any repeal legislation … must include repeal of the reductions in payments for hospital services embedded in the ACA.” Sounds reasonable to me, but maybe not to others because if Congress sends the money back, it will raise Medicare’s costs for the next decade and beyond, resulting in premium increases for Medicare enrollees across the nation, and shortening the lifespan of the Medicare Hospital Trust Fund (now solvent through 2028) by years. Sad! (Read this excellent Kaiser Health Policy Brief for more details on the impact of ACA repeal on Medicare.)

Fifth, why don’t you just fix the ACA exchanges instead of killing them?

A parable: Last summer, Alaska realized that premiums in its health exchange and individual health insurance market would be rising in 2017 by over 40 percent. In response, the Republican legislature established a state reinsurance pool to protect insurers against high losses; after passing the law, insurance companies dropped their premium increases to about 7 percent.

Some health insurance exchanges (i.e., California, New York, Massachusetts) are working well, and some are having high rate increase problems. These problems are fixable with sufficient political will to address them. The problem is that Republican lawmakers don’t want fixes – they want repeal. In 2014, 2015, and 2016, exchange premium increases were below projections. In 2017, they have risen at high rates in most states because of the end of rate protections known as “risk corridors” and “reinsurance” as well as the underfunding of “risk adjustment” in the ACA. All of these “3Rs” are permanent features of the Medicare Part D prescription drug program that Republicans support there and despise in the ACA.

These exchange problems are fixable. Yet you refuse to support them and fix the problems because that would undermine your case for ACA repeal.

These are my top five questions right now. Any answers, my friends?

PRESIDENT-ELECT DONALD TRUMP has nominated Rep. Tom Price of George, an orthopedic surgeon and the House Budget Committee chairman, to be his first secretary of health and human services. For those lulled into believing that Trump was moderating his views on the Affordable Care Act because of recent statements on 60 Minutes that he leaned toward supporting ACA provisions on banning pre-existing condition requirements and allowing young adults to stay on their parents’ insurance plans, this nomination is a bucket of ice cold water.

UNITED STATES – APRIL 16: Rep. Paul Ryan, R-Wisc., right, Chairman of the House Budget Committee, and Rep. Tom Price, R-Ga., prepare for a hearing titled “The President’s FY2014 Revenue and Economic Policy Proposals,” . (Photo By Tom Williams/CQ Roll Call)

Price, a leading member of the House GOP’s “doctor caucus,” and a founding member of the Tea Party caucus, has been a strident ACA critic from the start, issuing and reissuing his own ACA replacement plan – the “Empowering Patients First Act” – on several occasions. He has carved a role as House Speaker Paul Ryan’s strongest ally in proposing a radical reconstruction not just of the ACA but of the entire US health security landscape, seeking not just to obliterate President Obama’s health legacy, but also that of President Lyndon Johnson, who signed Medicare and Medicaid into law way back in 1965.

The Ryan-Price agenda includes four key components:

As far as possible, repealing the ACA’s private health insurance and Medicaid coverage expansions, along with most of the new taxes that finance them;

Reengineering the Medicare program into “premium support” in which enrollees will receive fixed dollar vouchers to purchase health insurance policies;

Reconstructing Medicaid into a “per capita allotment” financing model to drastically limit federal dollars to state governments that would be incentivized to limit eligibility and benefits to low income enrollees while increasing cost sharing; and

Capping the federal employer health insurance tax deduction that would sharply increase insurance costs for workers and their employers.

[The Q&A below was published in Harvard media this past week.]

How might the election of Donald Trump as the next U.S. president impact public health over the next four years? John McDonough, professor of the practice of public health at Harvard Chan School, who worked in the Senate on the passage of the Affordable Care Act (ACA), offers his perspective in this Q&A.

John McDonough

Many are worried that Obamacare will be in deep trouble—and likely be repealed—once Donald Trump is in the White House, working with Republican majorities in both the House of Representatives and the Senate. A week after the election, Trump appears to be hedging on his prior pledge to completely do away with the health reform law. What do you think will happen to the ACA—and to the millions of people who gained health insurance because of it?

The likelihood for total 100% repeal of the ACA is unlikely for two reasons: One is that this would have to be accomplished through regular legislative order in the U.S. Senate and Republicans would not be able to attract the necessary eight votes needed from Democratic senators to do this. Of course, if Republicans choose to abolish the filibuster, that would change. A second reason that repeal is unlikely is that many Republicans appreciate many non-controversial provisions in the ACA and repealing them would be backward steps they would not want to make happen.

Instead, and for now at least, Republicans appear to be moving toward a two-track process of “repeal and replace.” Repeal of the ACA’s essential health insurance coverage provisions, as well as the new taxes that financed the ACA’s expansions, could be achieved through the special “budget reconciliation process,” which only requires 51 votes for passage and cannot be filibustered. This would take some months to achieve, and is doable as long as 50 of the 52 Republican senators are willing to vote to eliminate coverage for as many as 22 million Americans—the number newly insured under the ACA—and their willingness to do that is not yet certain. Republicans did vote to repeal the most important parts of Obamacare in January of this year, but they did it knowing that President Obama would veto the measure. It would be a different vote knowing that President Trump would sign it.

Replacing the ACA with some other sort of health care law would be far more difficult because that legislation would need to proceed through regular legislative order and could and would be filibustered by Democrats, thus blocking the legislation. So it is conceivable that repeal could happen and replace might not follow, which would leave the up-to-22 million most at risk in a most difficult situation.

It’s been reported in the media that President-elect Trump may consider keeping some of the ACA’s more popular provisions, such as the requirement that insurance companies not deny coverage to people with pre-existing medical conditions, or that children up to age 26 can be covered under a family’s health plan. How do you think this might play out?

House Speaker Paul Ryan and House Republican leaders, in their “Better Way” document on repeal and replace last summer, indicated that they would continue the ACA’s “guaranteed issue” provisions—those making it illegal for insurers to deny anyone coverage because of health status, age, gender, or other factors—though only for those who are able to maintain “continuous coverage” with no or only short-term coverage breaks. For the millions of Americans who find themselves unable to afford coverage for some period of time, Republicans would, by their own words, return pre-existing condition exclusions and medical underwriting—charging the sick higher prices than the healthy. The provision for children up to age 26 being able to stay on parent’s health insurance policies is most likely not to be repealed.

How might the new president’s policies impact women’s health? He has said he would nominate a conservative Supreme Court justice who would be in favor of a pro-life agenda. Could this lead to Roe v. Wade being overturned? What other ways might women’s health be impacted under the Trump administration?

Even with a Trump appointment to the U.S. Supreme Court, there are five current votes, including Justice Anthony Kennedy, opposed to a Roe v. Wade repeal. So President Trump would need at least one additional replacement of those five to have a chance at repeal.

Other aspects of women’s health coverage are at risk because of Republican plans to repeal large portions of the ACA. Republicans want to return all discretion over required benefits to states, including the ACA’s mandates on benefits such as birth control, mammography, prescription drugs, behavioral health, and much more. So it’s possible that women could lose coverage for services that are currently free, such as contraception, mammograms, folic acid supplements during pregnancy, and screenings for gestational diabetes, sexually transmitted diseases, and cervical cancer.

Trump broke with conservative orthodoxy when he said that he’s in favor of Medicare being able to negotiate drug prices. He also has said that he would take on the Big Pharma lobby in order to reduce high prescription drug costs. Do you think he’ll be able to follow through on these pledges?

President Trump’s administration would only be able to negotiate drug prices or make other significant changes in pharmaceutical policies with the consent of Congress, which is most unlikely to provide that authority to him. Also, though the health policy section on his campaign website included drug-related proposals, the health policy section on his presidential transition website includes no mentions of these.

There were a number of health-related ballot initiatives across the nation. Three states, including Massachusetts, voted to legalize recreational marijuana and another three voted in favor of medicinal pot; voters in California, Washington, and Nevada approved various gun control measures; Californians raised cigarette taxes; and four cities voted to tax sugar-sweetened beverages. Also, Colorado rejected the establishment of a single-payer health insurance system in that state. How are these ballot initiatives changing the public health landscape?

On recreational marijuana, the tide of public opinion is changing the national landscape in spite of bipartisan opposition to this liberalization from elected officials all over the nation. It feels somewhat like the fast-changing tide a few years ago on gay marriage. And it feels unstoppable.

Taxes on sugar-sweetened beverages, at least on the local level, seem to be approaching the level of public acceptance we have seen in prior years with relation to tobacco taxes. The public seems supportive, at least in cities, especially when the revenues raised are clearly defined in terms of spending targets, such as public education. We have yet to see this approach pushed at a state initiative level, which would be a much more challenging proposition.

Regarding the vote against single-payer health insurance in Colorado, it seems that the U.S. sees one of these single-payer ballot initiatives every decade or so, and in each case, they start with some robust public support and then lose in a landslide: California in 1994, 73% to 27% no; Oregon in 2002, 77% to 23% no, and now Colorado in 2016, 80% to 20% no. It has always been a difficult sell and the Colorado results demonstrate that it still is.

The insurance of at least 22 million Americans hangs in the balance

The election of Donald Trump as 45th president of the United States has triggered concerns in many globally important areas of public policy, including climate change. But for Americans, one of the most unsettling challenges is the future of domestic healthcare policy and the fate of the 2010 health reform law, the Affordable Care Act (ACA).

For 45 years, the US healthcare system has been accurately characterized as the most expensive among nations in the Organization for Economic Cooperation and Development (OECD), as mediocre regarding quality and effectiveness, as inadequate in that it left nearly 50 million Americans uninsured, and as substandard in core outcomes such as infant mortality and life expectancy. In short, the only category at which Americans seemed to excel was in spending the most money.1

Between 2005 and 2008, many sectors in American society became vocal in calling for comprehensive healthcare reform to address failings in access, quality, cost, and outcomes. Between January 2009 and March 2010, new President Barack Obama worked with hefty Democratic majorities in the US Senate and House of Representatives to fashion comprehensive reform to tackle these deficiencies, signing the ACA on 23 March 2010. Though some Republican members of Congress initially expressed support for reform, objections to the Democratic approach and political resistance from their grassroots left zero Republican supporters by the time that the ACA was signed. Continue reading “Explaining our Health Care Dilemma to the World”

We are nearing the grand finale of our long and disheartening election opera, one we dare not ignore because the outcomes matter so much. While the election results will not be determined by public reactions to the Affordable Care Act, the ACA’s fate will be mightily determined by Tuesday’s outcomes. What have we learned about our collective health future over the past 18 months and what might this mean for our health system’s future?

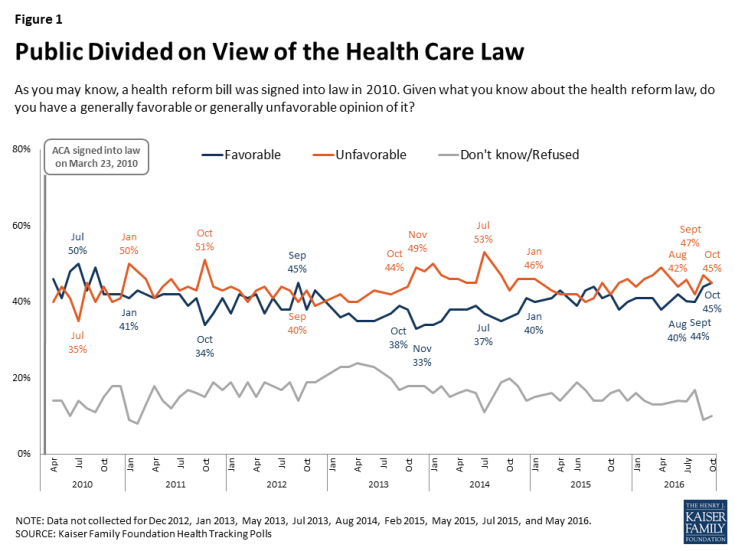

Public opinion on health reform is as frozen today as it was in spring, 2015

Kaiser monthly tracking polls show reliably unfavorable attitudes toward the ACA, slightly beating favorables, and stuck since 2014 in 40 percent purgatory. The advantages millions of Americans feel from ACA insurance coverage expansions and other access reforms are balanced by those who now blame the ACA for everything bad that happens in health care. The misnamed Pottery Barn rule—“if you break it, you own it”—applies here even though the dish was broken well before the ACA. Beyond this, if there is one thing on which both sides of the new Republican divide concur, it is a deep hostility towards ObamaCare. The election cycle seems to have only hardened these views.

The essential differences between Democrats and Republicans are now more clear

We know more about the preferences of both parties with respect to the ACA than we did 18 months ago. Hillary Clinton, Donald Trump, and House Speaker Paul Ryan, have released health reform planks that clarify their intentions — regardless of Congressional feasibility.

Clinton wants to maintain and strengthen the ACA by improving premium affordability and by addressing excessive cost sharing in the Exchanges and beyond. She has an eight-point plan to address pharmaceutical prices. She will emphasize women’s health, and much more. Her campaign has articulated the first full agenda of any leading Democrat to improve and advance the ACA, helping to define the arena of possibility, whether far-fetched or not.

After early teasing about his admiration for the Canadian and Scottish single-payer systems, Trump embraced standard Republican orthodoxy on ObamaCare, most recently announcing his intention to call a special Congressional session as soon as possible to repeal the law. Two independent research institutes (Committee for a Responsible Federal Budget and the Commonwealth Fund) have concluded that Trump’s agenda, if implemented, would result in 20 million Americans losing health insurance and would increase the federal deficit by $330-550 billion over 10 years.

Meanwhile, Speaker Ryan announced in September his intention—if Republicans control both houses of Congress and the White House in January—to expedite budget reconciliation legislation that would repeal as much of ObamaCare as possible. Though Ryan’s plan is more ambitious than Trump’s, of the latter’s seven health policy planks, five also show up on the Speaker’s agenda.

The final week’s fireworks over premium increases in the individual health insurance market only emphasize that the political volatility of the ACA/ObamaCare has not diminished at all.

Differences involving the ACA are not about facts or data, but about fundamental values

One of my favorite political scientists, Deborah Stone, in her book Policy Paradox, writes that much of the policy process involves debates about values masquerading as debates about data and facts. That sure describes the past eight years of health reform. As my colleague Robert Blendon showed in his pre-election special report for TheNew England Journal of Medicine:

The political parties fundamentally differ over the role the federal government should play in intervening in the U.S. health care system, (and) the desirability of the federal government moving ahead with future efforts aimed at universal coverage…

The notion that these differences might be leavened, for example, by changing the age-rating bands (the maximum amount an insurer can charge in premiums for young people versus older enrollees) in the Exchanges from three-to-one up to six-to-one, is delusional. Six and a half years after its signing, the ACA has yet to become settled policy because the differences are simply too deep and neither side of the political divide can risk the backlash of surrender.

Republicans don’t want to fix the ACA car at any cost; they are determined to smash it

The excessively high premium increases in 2017 in the ACA Exchanges, more than anything, are tied to elimination in 2017 of risk corridors and reinsurance, as well as the undermining of risk adjustment. This past summer, Alaska’s Republican Legislature established its own reinsurance mechanism to stabilize rates, and immediately saw premium increases drop from over 40 percent to under 10 percent.

In my time as a member of the Massachusetts House of Representatives (1985-1997), I learned that when political partners like and respect each other, the most difficult challenges could be met with seeming ease; and conversely, when parties disliked and disrespected each other, the easiest chores were impossible to achieve. And thus it is with the ACA Exchanges, eminently fixable technically, and utterly unfixable politically.

And ACA demolition is advanced with no clearly defined replacement alternative. Yes, Speaker Ryan advanced a health reform agenda this past summer; yet he and his team did not put their ideas into legislative language that could be scored by the Congressional Budget Office, perhaps because they knew that the results on both lost insurance coverage and rising costs would turn the public against them.

As I write this on November 3rd, the most likely outcome from November 8 is divided government, with a Senate majority hanging by a thread. (Please recall that Senator Al Franken (D-MN) took his U.S. Senate seat for the first time in July 2009 after an eight-month recount process.) Republicans know that the electoral map in 2018, all things being equal, will offer substantial gains in both the Senate and the House, particularly if their political base is pleased. Democrats know that they will need to deliver on at least some of their promises, and not allow the signal accomplishment of the Obama Administration to fall apart.

Dare I say it: we’re going to need some statesmanship at a time when that commodity is in short supply.

The commentary below was published in JAMA Internal Medicine online on October 10 2016 and was written by me and David K. Jones from the Boston University School of Public Health:

Although the outcomes of the US Presidential and Congressional elections in November 2016 will not be determined by attitudes toward the Affordable Care Act (ACA), the results will likely determine its long-term fate. As was the case in 2008 and 2012, the electorate’s decisions on whether the Republicans or the Democrats control the White House, the Senate, and the House of Representatives will have fundamental consequences for the future of national health reform.

A Republican victory that includes that party’s control of the White House, Senate, and House of Representatives would likely augur huge shifts in national health policy. A Democratic victory that included the White House and a Senate majority would likely further embed the ACA into state and federal health policy, and perhaps lead to further expansion and reforms. More than 6 years after President Barack Obama signed the legislation into law in 2010, the ACA has yet to become settled policy.

The Republican Agenda

Over the past 4 years, Republican members of Congress and conservative think tanks such as the American Enterprise Institute and the Manhattan Institute have advanced numerous proposals to repeal and replace the ACA. As the final stages of the 2016 campaign approach, 2 plans stand out: Republican presidential candidate Donald Trump’s agenda as outlined on his campaign website,1 and the House Republican leadership plan released by Speaker Paul Ryan (R-WI) in June 2016.2 Continue reading “The Choices on Health Reform in the US Presidential and Congressional Elections”

“Donald Trump’s plan to repeal and replace Obamacare would cost nearly $500 billion over a decade, or $270 billion incorporating economic growth.

“The plan would nearly double the number of uninsured, causing almost 21 million people to lose coverage.”

To my knowledge, this is the first serious and independent economic analysis of any Republican or conservative health reform plan released since the Affordable Care Act (ACA) was signed in 2010. It’s not a pretty picture.

In addition to “completely repeal(ing) Obamacare,” Trump’s proposal would:

Allow sale of health insurance across state lines;

Allow individuals to fully deduct health insurance premiums from their income tax obligations;

Allow individuals to use Health Savings Accounts;

Require transparency from all health care providers;

Block grant Medicaid to the states;

Remove barriers to entry into free markets for drug providers.