Once upon a time, I believed that efforts to repeal the Affordable Care Act (ACA) would wither and die once the ACA’s major Medicaid and private insurance expansions became effective on January 1, 2014. After all, opponents had let Senator Ted Cruz (R-TX) trigger a 3-week federal government shutdown in October 2013 in a desperate final attempt to thwart the expansions. Over the course of 2 open enrollment periods, between 2013 and 2015, as many as 17 million previously uninsured Americans obtained coverage. Surely the worst was over. Now I am not so certain.

Since 2010, Americans have witnessed 3 near-death experiences relating to national health reform: first, the election of Scott Brown (R-MA) to the US Senate in January 2010, ending Democrats’ 60-vote filibuster-proof majority; second, the US Supreme Court’s decision in June 2012 upholding the constitutionality of the ACA writ large; and third, the November 6, 2012, federal elections in which a victory for presidential candidate Mitt Romney would have augured substantial repeal. By this standard, the October 2013 government shutdown and the 2015 Supreme Court case, King v Burwell, were faux near-death experiences, not the real thing. Continue reading “Is the Fate of the ACA Settle or Not?”

A new website called “The Conversation” posted this article earlier today:

If the leading Republican candidates agree on one thing, it’s doing away with Obamacare.

“The one thing we have to do is repeal and replace Obamacare,” Donald Trump has written on his campaign website, while Marco Rubio has outlined his plan to “Repeal Obamacare” and “replace it with a 21st century, market-driven alternative.” Likewise, Senator Ted Cruz emphatically declared during the February 25 GOP debate that “As president, I will repeal every word of Obamacare.”

Is this the bombastic rhetoric of candidates trying to fire up their base? Or would Republicans actually be able to repeal Obamacare under a Republican president?

In short: yes, they could. But it wouldn’t be easy.

The main GOP obstacle

The essential requirement to achieve repeal is Republican control of the White House, the U.S. Senate and the House of Representatives in January 2017.

Unless both houses of Congress and the executive branch are under GOP control, Democrats would be able to block any repeal effort – and the Obamacare trench warfare that’s taken place since Democrats lost control of Congress in January 2011 would continue.

But even if Republicans control Congress and the White House, Senate Democrats could filibuster any legislation that repeals Obamacare.

Sixty senators must vote to close a filibuster – a Senate parliamentary tool designed to protect the rights of senators to slow or stall legislation and other matters. While, historically, filibusters took the form of long speeches on the Senate floor, these days it’s a less heroic procedural maneuver.

It’s unlikely that Republicans will have a 60-vote majority in the Senate in 2017. Meanwhile, Senate Democrats have been unanimous against repeal, and the number of Democrats in the chamber next year is predicted to increase over their current 46.

For this reason, even in if they’re in the minority, Democrats could block any straight repeal legislation and compel Republicans to resort to another path.

Skirting the filibuster with reconciliation

Republicans could then initiate an arcane legislative process called budget reconciliation. Invented in 1974 by the late West Virginia Senator Robert Byrd (arguably the shrewdest legislative tactician ever), budget reconciliation is a special legislative process that enables federal budget bills to be approved in an expedited fashion.

Reconciliation is the brainchild of West Virginia Senator Robert Byrd.Wikimedia Commons

The advantage of reconciliation is that it permits a bill to be approved by 51 votes. (If Republicans hold 50 votes in the new Senate – a possibility – a Republican vice president can provide the 51st vote.)

Since reconciliation bills cannot be filibustered, any Obamacare repeal bill done using reconciliation wouldn’t need a 60-vote majority to proceed. And debate on a reconciliation bill is limited to 20 hours. For a frustrated Senate that doesn’t have a 60-plus vote filibuster-proof majority, it’s the most potent legislative shortcut imaginable.

But there’s a vital catch: any item in a reconciliation bill must have a measurable, direct impact on federal spending, up or down.

The individual who decides what legislative items do and do not conform to this rule is the Senate parliamentarian – the individual tasked with advising Senate leaders on the interpretation of Senate rules. Appointed by the Senate majority leader whenever the prior parliamentarian steps down, a former Senate librarian clerk named Elizabeth MacDonough currently holds the position.

A full ACA repeal bill would be deemed noncompliant by MacDonough and set aside because so many of its individual provisions do not have a significant budget impact. In a process known as the “Byrd bath,” Senators can challenge any entire bill, section, subsection, paragraph, sentence or word as “out of order,” meaning there is no significant budget impact. Items eliminated by the parliamentarian – called “Byrd droppings” – are removed from the bill.

But could Republicans then devise a partial – and critically damaging – ACA repeal bill that might pass muster with MacDonough or her successor?

Yes, they can. In fact, they’ve already done so.

GOP shows it can be done

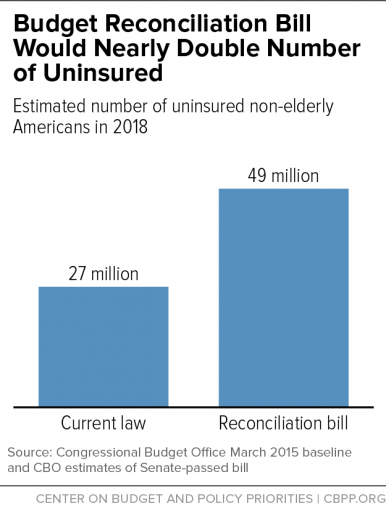

This past December and January, the Senate and the House passed a reconciliation bill that would have repealed fundamental building blocks of Obamacare, including subsidies to help moderate-income Americans afford health insurance and funds to expand Medicaid to low-income, uninsured individuals.

The Congressional Budget Office reviewed the proposal and determined that it would cancel insurance coverage for about 22 million Americans by 2018.

When the bill reached President Obama’s desk, he vetoed it. On February 2, Groundhog Day, the House failed to override his veto – their 63rd vote to repeal all or part of the ACA – voting almost completely along party lines.

Some observers declared that vote a waste of time because the outcome was known from the outset. This is erroneous.

A bill repealing crucial building blocks of Obamacare sits on a desk after being signed by U.S. House Speaker Paul Ryan on January 7, 2016.Jonathan Ernst/Reuters

Prior to the reconciliation bill passing the Senate this past December, many, including Senate Minority Leader Harry Reid, confidently predicted that Republicans would never successfully navigate the treacherous and confounding reconciliation waters.

But they did.

As a result, congressional Republicans have demonstrated that they can achieve effective deconstruction and de facto ACA repeal using reconciliation. It’s no longer an idle threat.

Every 2016 Republican presidential candidate has publicly declared his or her support for complete ACA repeal. Of the eight ACA replacement plans advanced by members of Congress and conservative think tanks, all but one presume total or near total repeal. And it’s difficult to identify more than a handful of Republican members who express any reservations about repeal.

So if there were a Republican president in Obama’s place, could a GOP-controlled Congress repeal the ACA early next year?

Maybe and maybe not.

A Senate majority in flux

It’s likely that Republicans will return to the Senate next January with fewer than their current 54 votes – and may even lose their majority.

That is because, in recent times, presidential election years have attracted more Democrats and liberals than midterm election years, which tend to result in more Republican, conservative leaning outcomes. Furthermore, Democrats have had notable success so far this cycle recruiting their top choices in key battleground states. Wisconsin Senator Russ Feingold is running for his old seat, while New Hampshire Governor Maggie Hassan now running against incumbent Republican Senator Kelly Ayotte.

Even more important, some Republicans appear to have supported January’s reconciliation bill precisely because they knew it would never become law.

One example is West Virginia Senator Shelley Moore Capito. Capito made it clear that she did not want to take Medicaid away from 160,000 low-income West Virginians. Other more moderate Republican senators – Maine’s Susan Collins, Illinois’ Mark Kirk, and New Hampshire’s Kelly Ayotte – might also think twice about voting to eliminate health coverage for vulnerable constituents for real.

Since President Obama signed the ACA in 2010, Republican Congressional leaders, especially House Speaker Paul Ryan, have cockily promised to move legislation to replace Obamacare.

It’s been six years of broken promises with their latest replacement show now underway. One reason for their inability is deep disagreement within the Republican conference about what could replace the ACA.

While Republicans find it easy to vote to repeal the law, their consensus vanishes when the topic turns to replacement. Look no further than the GOP debates, where candidates have been unable to articulate a consistent vision for health care policy beyond allowing the sale of health insurance across state lines and expanding high deductible health insurance policies.

So if Republicans capture the White House, Senate and House, will they repeal the ACA?

Six years after the Affordable Care Act (ACA) became law, U.S. health care policy and the delivery of medical services continue to undergo unprecedented change. Rockland Trust’s “Talking Business Advice Series” spoke with John E. McDonough, professor of Public Health Policy at the Harvard T.H. Chan School of Public Health, to get his take on what may lie ahead for businesses working with the ACA during this dynamic period.

Q: You helped write the ACA. It’s an extremely complex law that even today is not fully understood by many Americans, including business owners and leaders. From a high-level perspective, where do things stand with it today?

A: Most people understand that the ACA is moving us toward universal health coverage. For the United States, the ACA is a revolution, an enormous set of changes that many see as a huge step forward and many others see as a wrong turn. Globally, however, all of the world’s advanced nations prior to the ACA already had health care schemes that, to varying degrees, met the insurance needs of their populations. So, while the ACA’s insurance expansions and reforms represent a great leap forward for the U.S., it is also true that when fully implemented by 2018, the U.S. will still have the most inefficient, wasteful, and unfair health insurance system of any advanced nation, even with the ACA reforms.

On the other hand, the ACA is also advancing an agenda of dramatic and necessary change in how medical care is delivered in the U.S. As a nation, we are now moving rapidly away from a financing system based on fee-for-service payments, (which is) a system that rewards hospitals, physicians, and other medical providers based on the quantity of services they provide without regard for the quality, effectiveness, and efficiency of those services. Because of the ACA, we are now moving quickly toward a new financing framework that rewards hospital, physicians, and providers based on the quality and value of the services they provide rather than the quantity.

Q: The public doesn’t necessarily view it in this way, does it?

A: You’re right. This change has gone unrecognized by the broad public, even as it moves forward in rapid and profound ways. A lot of what the ACA envisions is experimental. Some elements are working better than others; some continue to be fiercely debated. The U.S. doesn’t have all the answers in this effort, but we have the most dynamic set of experiments on this evolutionary path of any advanced nation on the planet right now. Health system leaders all around the world are very interested in this set of experiments and watching closely. That is something that corporate leaders, regardless of industry sector, ought to recognize, appreciate, and understand.

Q: What are some of the effects of these experiments on businesses?

A: The immediate effects of the ACA depend on the context of the business itself. For example, the ACA’s impact is different for larger businesses with more than 50 full-time workers, companies with new responsibilities under the ACA’s employer mandate. It’s different for smaller employers and it provides some opportunities for many of them. It’s a unique new context for start-up businesses because of the health insurance marketplaces that provide new businesses with a new way to provide health insurance for their workers, enabling them to outsource their health coverage needs for themselves and their employees. And it enables all employees to get health care coverage regardless of pre-existing conditions, which was not possible in 45 states prior to the ACA.

So it’s contextual. It depends on the size and nature of the business as to whether there will be advantages or disadvantages—or both—to the Affordable Care Act.

Q: Would you expand on how smaller companies can outsource their health care responsibilities?

A: The ACA required the development of government-regulated health care exchanges (or marketplaces) across the nation. States had right of first refusal and 13 have chosen to establish their own exchanges while the rest are run by the U.S. Centers for Medicare and Medicaid Services (CMS). These exchanges offer coverage to all eligible individuals who can’t obtain insurance elsewhere, and many workers are eligible for financial subsidies to keep premiums and cost sharing affordable.

Alongside these public exchanges, new private health insurance exchanges have emerged. Unlike the public exchanges, which largely provide insurance to individuals seeking to buy non-group coverage, these private entities are aimed straight at the employer community. These private exchanges can enable employers to address their responsibilities under the ACA’s mandate to provide health insurance for their workers and do it in ways that are far less onerous for employers than in the past. It’s a way to outsource these responsibilities and to provide employees with a range of coverage choices. This is a significant change from the environment that existed prior to the ACA’s passage in 2010.

Q: How are larger businesses affected by the ACA?

A: Prior to the ACA’s passage, larger businesses were concerned about not being heavily shaped by the new law because most of these businesses already covered most of their employees. The impact of the ACA on larger businesses—especially those that self-insure—is far less than what they would experience in the standard commercial insurance market were they to go out and purchase traditional coverage.

Nonetheless, there are important new coverage requirements that impact the large employer market—whether self-insured or not. For example, lifetime or annual benefit limits on workers coverage is no longer permitted. Employer plans must cover the “essential health benefits” specified in the law. A worker’s insurance premium cannot exceed 9.5 percent of his or her household income or else the employer mandate penalty can be triggered. All employers must allow their workers to keep adult children on their family policies up to age 26. The ACA also sets a 90-day maximum waiting period before full-time workers are eligible for coverage.

There are also some elements of the law that many employers appreciate, including the ability to vary worker premiums by 30-50 percent in relation to workers’ use of tobacco products and participation in workplace wellness programs. Clinically proven preventive care services, such as mammography, must be provided to workers without any cost sharing.

The ACA’s impact is far more substantial in the traditional commercial health insurance market—but the impact on large self-insured employers is also meaningful.

Q: Are all the details of the ACA settled at this point?

A: This law is changing every day. There are at least three dozen things changing in relation to this law almost daily—in Congress, in federal agencies, in states, in the private sector—changes shaping how this law is unfolding across American society. And the pace of change hasn’t slowed, even now when we’re in the sixth year since the law was enacted.

The ACA is likely to change even further next January when a new president and administration takes office, regardless of which party controls the White House and Congress. We can see an evolving agenda for changes from both sides of the political spectrum. Congressional Republicans have been united in their determination to dismantle the ACA for some time. In January, President Obama vetoed an attempt to cripple the ACA that was included in a budget reconciliation bill. The fact that this initiative passed Congress demonstrates that if Republicans control the White House, House, and Senate next January, there is a strong likelihood of significant dismantling of the law.

Conversely, if the Democrats hold the White House next year they also will have an agenda for significant changes to the ACA, though far less dramatic than what would happen under Republican control. Either way, we can anticipate some significant changes coming in 2017.

Q: How do business leaders prepare for that?

A: They need to keep abreast of whatever changes occur. Many organizations help businesses to stay on top of what’s changing or likely to change. It’s important for executives and managers who focus on a company’s health coverage to stay up-to-speed on what’s happening, and it’s important for those in the C-suite to understand the changes to factor these new variables into their strategic planning calculus.

As a nation, we are on a path of rapid and deep systemic change to our health system, and it’s going to unfold for some time to come. It is already transforming the fundamental nature of the U.S. medical care delivery system. The implications of it are vast and it will continue to unfold well into the future in positive, not-so-positive, and surprising ways.

It’s important for corporate executives to understand the nature of these changes as they happen.

The Harvard T.H. Chan School of Public Health will present a conference titled “Beyond the Affordable Care Act: The Next Frontiers for US Health Reform” on April 25-27. Visit https://ecpe.sph.harvard.edu/ for more information.

It’s funny how things turn out on the campaign trail. Since all Republican presidential candidates pledge to repeal the Affordable Care Act/ObamaCare, they have little to argue about. The fireworks are among Democrats as Hillary Clinton and Bernie Sanders argue the future of US health reform and, specifically, the merits of Sanders’ new single payer/Medicare for All scheme, released Sunday evening hours before the Democrats’ final pre-primary debate.

Clinton, fighting a Sanders surge in the Iowa and New Hampshire Democratic primaries, has been landing punches to throw his momentum off balance. Meanwhile, Sanders keeps humming the single payer tune that the Democratic base adores (see the Kaiser Poll below), offering some new melodies and riffs in his revised plan.

Sanders’ proposal matters because it shows how progressive thinking has shifted and because it calls into question whether Democrats have the staying power and political will to defend one of their principal accomplishments in the past 50 years, the ACA. Here are key points about the Sanders plan: Continue reading “Bernie Sanders and Hillary Clinton on Health Care – Who’s Got the Plan?”

The U.S. Senate approved the same bill in December and the House adopted it yesterday with no changes, so it is heading to the White House where President Obama is certain to veto the measure. The likelihood that House or Senate Republican leaders could summon the needed votes to override that veto is zero.

It’s easy to dive into the political games involved in this legislation because there are so many. Doing so, though, ignores our responsibility to recognize what this Congress has done – put itself on record to cancel health insurance for tens of millions of Americans and offer nothing, zero, to mitigate the harm to mostly low and lower middle income families.

Here are the bill’s key elements:

Eliminate the ACA Medicaid expansion

Eliminate the ACA’s premium and cost sharing subsidies to help lower middle income Americans buy private health insurance

Repeal the ACA’s individual mandate which helps to ensure a healthy risk pool of enrollees to keep premiums affordable

On one thing all Affordable Care Act watchers can agree: This autumn saw important developments and changes relating to the nation’s health reform law. How much and how serious? Any immediate assessment is incomplete and the full impact only will be evident through the lens of the 2016 presidential and Congressional election results. Until then, some impacts are clear. So let’s consider…

First, what has happened? Here is my list of key developments:

Congress delayed or suspended for one or two years the operation of three taxes that help finance the ACA: the so-called “Cadillac tax” on high-cost employer-sponsored health insurance policies; the medical device industry tax; and the health insurance provider tax.

The House and Senate are close to final agreement (coming in January) to use the budget reconciliation process to repeal major, critical portions of the ACA, legislation that President Obama will veto and will see his veto sustained.

14 of 23 co-op health insurance plans created from the ACA have collapsed; also, UnitedHealthcare is dropping out of the ACA market.

The third Open Enrollment process is proceeding smoothly with larger than expected numbers signing up for coverage – final numbers yet to come.

On Medicaid, more holdout states are warming up to accepting the ACA expansion, and Kentucky’s new Tea Party governor has abandoned his campaign commitment to repeal that state’s expansion.

More and more experts, from both sides of the ACA divide, are advancing robust and noteworthy proposals for ACA replacement or improvement.

[This post was originally published on December 4th on the Health Affairs Blog. It was co-written by me and Max Fletcher, a student at the Harvard TH Chan School of Public Health.]

The November 3 election of Matt Bevin as governor of Kentucky will provide an important indication of the seriousness of Republican intentions to undermine and repeal the health insurance expansions of the Affordable Care Act (ACA). Early in Bevin’s campaign, he expressed unambiguous intent to repeal Governor Steve Beshear’s executive order that expanded Medicaid; during the general election campaign, Bevin backpedaled and proposed adopting an Indiana-like Medicaid waiver to require significant enrollee cost sharing and an enrollment freeze. Bevin also prefers to close the successful Kynect health insurance exchange and transfer operating duties to the U.S. Department of Health & Human Services.

Whatever the outcome, the moves by the Tea Party-endorsed new governor will provide the best preview of what the nation may expect if Republicans take control of the White House and retain majorities in the Senate and the House of Representatives in January 2017. Many eyes will watch Governor Bevin’s health care moves from across the political spectrum. Continue reading “The $879 Billion Footnote — And The Financing Path To ACA Repeal”

For the 61st time since 2011, Congressional Republicans are moving legislation to undermine and dismantle key elements of the Affordable Care Act (ACA). This time, though, will be different.

First, this will be the first time Republicans will use the budget process known as “reconciliation” to advance repeal. Using a budget reconciliation bill prevents Democrats from filibustering the legislation in the Senate, meaning only 51 votes are needed for passage in expedited debate.

Second, this will be the first time that the House and Senate both pass similar legislation to damage the law. As a result, this will be the first time that anti-ACA legislation will reach President Barack Obama’s desk. The President’s veto of this measure is guaranteed, as are the needed votes in the House and Senate to sustain his veto. So this will be another exercise in ObamaCare-Kabuki Theater with some new twists.

(This article was published on Friday, September 18 on the Health Affairs Blog. It was prepared by me and Max Fletcher, a Master of Public Health student at the Harvard TH Chan School of Public Health.)

A new spate of proposals from Republican presidential candidates to repeal and/or replace the Affordable Care Act (ACA) raises the important question: Given an unobstructed opportunity, what would Republicans really do with the Affordable Care Act? Would they repeal the law wholly or just in part? With what might they replace it?

Some suggest that Republican Congressional leaders only advance full repeal to placate their Party’s conservative base, knowing well that repeal cannot survive a certain veto while Barack Obama is President. In January 2017, that obstacle will vanish if Republicans control the White House and both branches of the U.S. Congress. What then?

Unfortunately, the proposals now being advanced by the Presidential candidates are far less than comprehensive, and leave many more issues unanswered than answered.

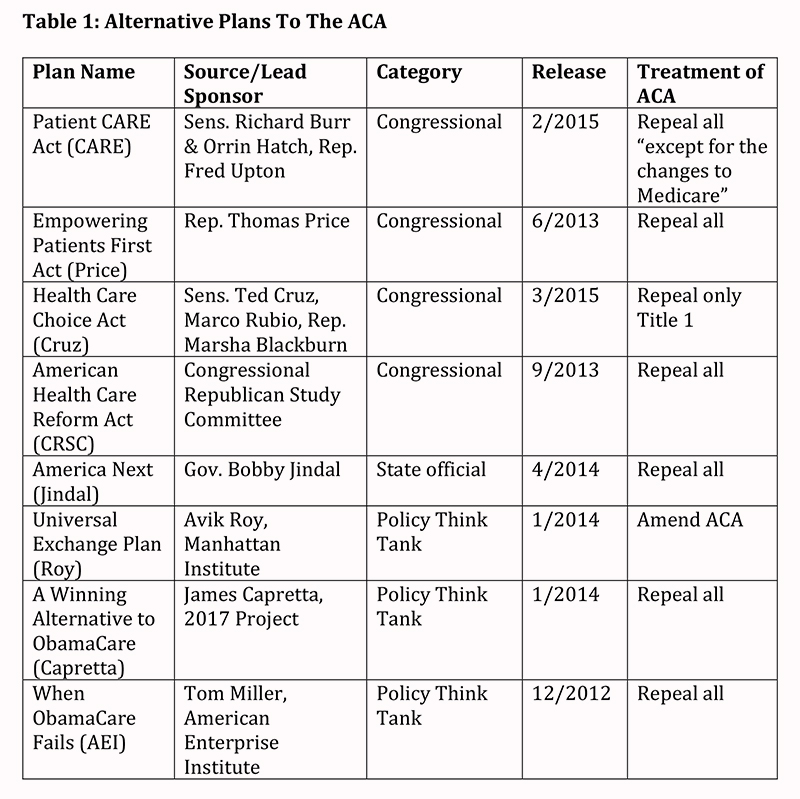

Though no ACA replacement plan has progressed in either branch (or in any standing committee) of Congress since the law’s 2010 signing, Republican office holders and conservative think tanks have advanced expansive proposals. We identified eight plans offered between 2012 and 2015 that address the ACA’s fate and propose substantive replacement. We examined each in detail to determine the extent of agreement on alternatives to the ACA. We created a chart comparing the eight proposals according to key policies. Table 1 below provides identifying information about the eight plans:

Of the eight proposals, four were advanced by Republican Members of Congress. The most prominent of these is the Patient CARE Act offered by Sens. Richard Burr (R-NC) and Orrin Hatch (R-UT) and Rep. Fred Upton (R-MI); the latter two are the current chairmen of the Senate Finance Committee and the House Committee on Energy and Commerce respectively, both committees with primary ACA jurisdiction. Though narrative versions of Burr-Hatch-Upton were released in 2014 and 2015, the authors have not translated their proposal into legislative language that can be evaluated by the Congressional Budget Office (CBO). While the other Congressional proposals have been introduced as legislation, none have received CBO scores. Continue reading “What Would Republicans Do Instead of the Affordable Care Act?”

A provision of the Affordable Care Act popularly – or unpopularly – known as the “Cadillac Tax” is getting lots of attention now, even though it doesn’t take effect until 2018. Voices from both parties want quick repeal. And the politics are strange.

Briefly, the tax is a 40% excise on high cost health insurance policies that cost more than $10,200 for individuals and $27,500 for families in 2018. It’s 40% on the increment, so an individual policy costing $11,200 would cost an extra $400. It was included to help finance the ACA’s cost and to apply pressure where it hurts the most to restrain the cost of health insurance.

When the ACA was signed into law in 2010, many critics asked: “where’s the cost containment?” One answer was: “the Cadillac tax.” The frequent response was derisive laughter: “The tax doesn’t hit until 2018 and it will be repealed well before then.” No laughter now. Continue reading “The Curious Politics of the “Cadillac Tax””

A: The immediate effects of the ACA depend on the context of the business itself. For example, the ACA’s impact is different for larger businesses with more than 50 full-time workers, companies with new responsibilities under the ACA’s employer mandate. It’s different for smaller employers and it provides some opportunities for many of them. It’s a unique new context for start-up businesses because of the health insurance marketplaces that provide new businesses with a new way to provide health insurance for their workers, enabling them to outsource their health coverage needs for themselves and their employees. And it enables all employees to get health care coverage regardless of pre-existing conditions, which was not possible in 45 states prior to the ACA.

A: The immediate effects of the ACA depend on the context of the business itself. For example, the ACA’s impact is different for larger businesses with more than 50 full-time workers, companies with new responsibilities under the ACA’s employer mandate. It’s different for smaller employers and it provides some opportunities for many of them. It’s a unique new context for start-up businesses because of the health insurance marketplaces that provide new businesses with a new way to provide health insurance for their workers, enabling them to outsource their health coverage needs for themselves and their employees. And it enables all employees to get health care coverage regardless of pre-existing conditions, which was not possible in 45 states prior to the ACA. The ACA is likely to change even further next January when a new president and administration takes office, regardless of which party controls the White House and Congress. We can see an evolving agenda for changes from both sides of the political spectrum. Congressional Republicans have been united in their determination to dismantle the ACA for some time. In January, President Obama vetoed an attempt to cripple the ACA that was included in a budget reconciliation bill. The fact that this initiative passed Congress demonstrates that if Republicans control the White House, House, and Senate next January, there is a strong likelihood of significant dismantling of the law.

The ACA is likely to change even further next January when a new president and administration takes office, regardless of which party controls the White House and Congress. We can see an evolving agenda for changes from both sides of the political spectrum. Congressional Republicans have been united in their determination to dismantle the ACA for some time. In January, President Obama vetoed an attempt to cripple the ACA that was included in a budget reconciliation bill. The fact that this initiative passed Congress demonstrates that if Republicans control the White House, House, and Senate next January, there is a strong likelihood of significant dismantling of the law.

{kind=link}