(This article was published on Friday, September 18 on the Health Affairs Blog. It was prepared by me and Max Fletcher, a Master of Public Health student at the Harvard TH Chan School of Public Health.)

A new spate of proposals from Republican presidential candidates to repeal and/or replace the Affordable Care Act (ACA) raises the important question: Given an unobstructed opportunity, what would Republicans really do with the Affordable Care Act? Would they repeal the law wholly or just in part? With what might they replace it?

Some suggest that Republican Congressional leaders only advance full repeal to placate their Party’s conservative base, knowing well that repeal cannot survive a certain veto while Barack Obama is President. In January 2017, that obstacle will vanish if Republicans control the White House and both branches of the U.S. Congress. What then?

Unfortunately, the proposals now being advanced by the Presidential candidates are far less than comprehensive, and leave many more issues unanswered than answered.

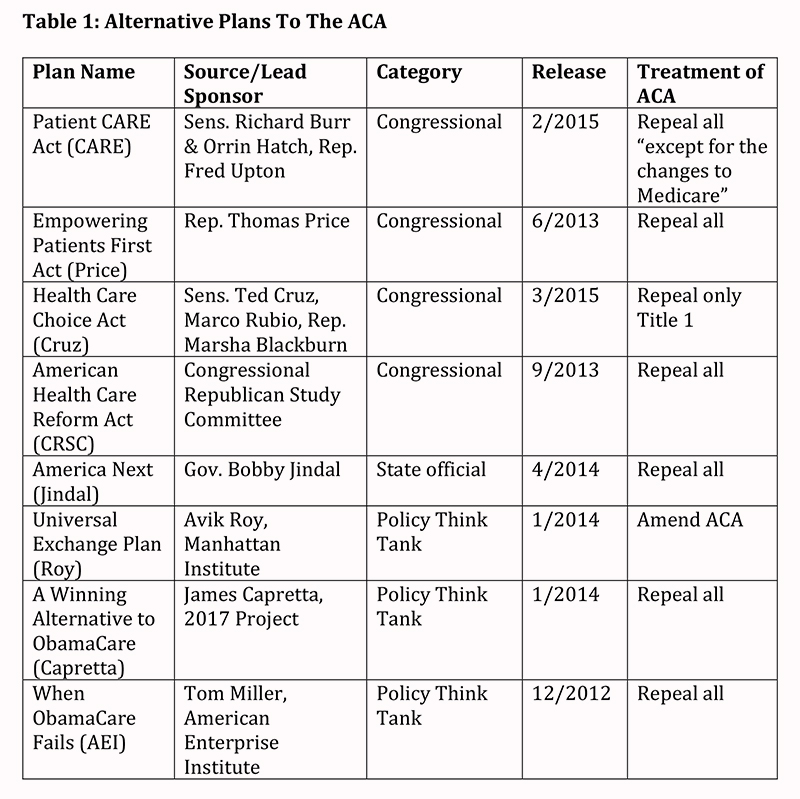

Though no ACA replacement plan has progressed in either branch (or in any standing committee) of Congress since the law’s 2010 signing, Republican office holders and conservative think tanks have advanced expansive proposals. We identified eight plans offered between 2012 and 2015 that address the ACA’s fate and propose substantive replacement. We examined each in detail to determine the extent of agreement on alternatives to the ACA. We created a chart comparing the eight proposals according to key policies. Table 1 below provides identifying information about the eight plans:

Of the eight proposals, four were advanced by Republican Members of Congress. The most prominent of these is the Patient CARE Act offered by Sens. Richard Burr (R-NC) and Orrin Hatch (R-UT) and Rep. Fred Upton (R-MI); the latter two are the current chairmen of the Senate Finance Committee and the House Committee on Energy and Commerce respectively, both committees with primary ACA jurisdiction. Though narrative versions of Burr-Hatch-Upton were released in 2014 and 2015, the authors have not translated their proposal into legislative language that can be evaluated by the Congressional Budget Office (CBO). While the other Congressional proposals have been introduced as legislation, none have received CBO scores.

Extent Of Repeal

Five plans propose complete ACA repeal without exception. The Patient CARE Act would repeal the entire law “except for the changes to Medicare” without elaboration. Sen. Cruz’s legislation would repeal only Title I. Only the Roy proposal would modify policy within the existing ACA statute. Beyond these eight plans, the fiscal year 2016 budget resolution, approved in May by exclusively partisan majorities in the U.S. House and Senate, includes explicit instructions for full ACA repeal.

What Would Come Next?

Based on these plans, we conclude that a Republican-controlled federal government would seek full or nearly full ACA repeal and attempt to start over with new policies. What new policies would likely be included or not? To clarify this discussion, we relate each substantive element of the ACA to its respective title in the statute:

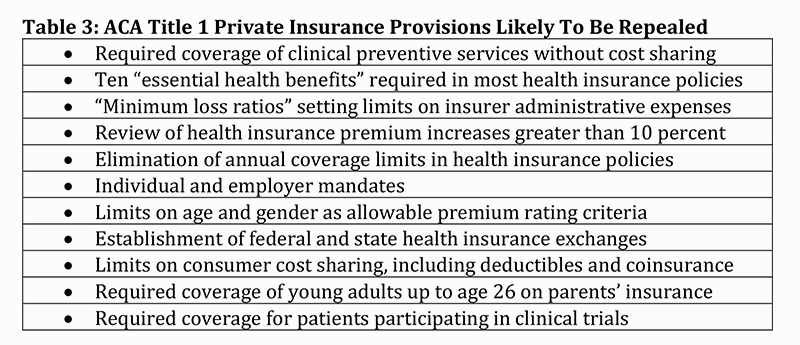

Title 1 (Private Health Insurance)

Under at least seven proposals, most ACA provisions that regulate the practice of health insurance would be repealed, as identified in Table 3:

What policies might they seek to implement instead? All of the Republican plans but one include some form of financial support to help consumers pay premiums, though no consensus exists on the form of that support. Five propose limited tax credits while two endorse more limited tax deductions. All are substantially less generous than the ACA’s premium tax credits. All plans but one would eliminate the ACA’s financial subsidies that limit excessive consumer cost sharing. All but two propose expansion of high-deductible Health Savings Accounts (HSA).

Regarding guaranteed issue, medical underwriting, and pre-existing condition exclusions in health insurance policy rating, while all plans endorse the principle of guaranteed issue, all but one require that individuals have at least 12-18 months of continuous coverage to avoid medical underwriting. Though two plans preserve the ACA’s ban on lifetime benefit limits in insurance, six do not, and all but one (Roy) eliminate the ACA’s ban on annual benefit limits.

Six plans would permit the sale of health insurance across state lines and promote re-establishing state high-risk pools for individuals with pre-existing conditions. All plans but one address medical malpractice reform, though without consensus on how: four propose mandatory federal caps on non-economic damages, and three propose tribunals or other new mechanisms.

In summary, the plans demonstrate a clear intent to deregulate most consumer protections established in the ACA, and to eliminate the individual and employer mandates. More limited tax-based assistance would be available to fewer consumers and that assistance would not vary by income. Guaranteed issue and the elimination of pre-existing condition exclusions would apply only to individuals who can maintain continuous coverage. Some form of malpractice reform would likely be included.

Title 2 (Medicaid)

Seven plans would eliminate the ACA’s Medicaid expansion to families with incomes under 138 percent of the federal poverty line. Regarding a replacement, no consensus appears. Two plans endorse converting Medicaid into block grants for states; others allow low-income families to use limited and non-income based tax credits or deductions; one establishes HSA-like Medicaid Opportunity Accounts.

Plans also propose sweeping changes for all or most pre-ACA Medicaid eligibility categories. Only two plans would preserve existing arrangements for aged, blind, and disabled enrollees; all others are silent on this point.

Title 3 (Medicare and Delivery System Reform)

This central ACA title contains two sets of policies: first, improved benefits for Medicare enrollees coupled with spending reductions to providers (except physicians) to help finance Titles 1 and 2 coverage expansions; and second, initiatives to improve the quality, efficiency, and effectiveness of medical care.

Five plans would repeal Title 3 entirely. One would repeal the entire ACA “except for the changes to Medicare.” These plans would repeal all Title 3 delivery system reforms, such as:

- accountable care organizations;

- the Center for Medicare and Medicaid Innovation;

- bundled payment demonstrations;

- hospital penalties for high rates of Medicare patient readmissions and health care associated conditions;

- the Independent Payment Advisory Board;

- and Medicare Advantage quality incentives.

No consensus is evident regarding the future of Medicare beyond repealing the ACA provisions.

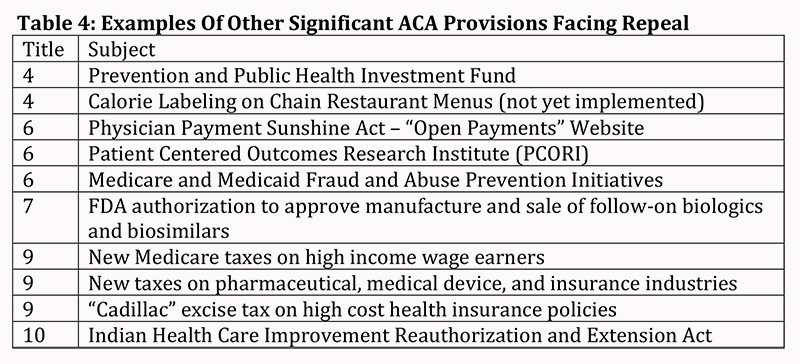

Titles 4-10

Titles 4-10 includes provisions across numerous policy domains including:

- prevention and public health;

- health care workforce;

- fraud and abuse;

- provider transparency;

- clinical comparative effectiveness;

- the Indian Health Service;

- authorization for the manufacture and sale of biosimilar biopharmaceuticals;

- plus provision for new taxes to finance a substantial part of the ACA.

Six proposals would repeal all these titles in toto. Table 4 lists significant changes that would occur with the elimination of these provisions:

Financing Repeal

Financing, of course, is a crucial consideration in any Congressional action. A June analysis by the CBO determined that full ACA repeal would increase the federal deficit over the 2016-25 decade by $137 billion to $353 billion. Importantly, the Burr-Hatch-Upton Patient CARE Act would retain Title 3’s Medicare payment reductions, thus providing an estimated $879 billion in retained revenue that could be used to repeal the rest of the ACA in a deficit-reducing fashion. If indeed there is a path to repealing the ACA that also reduces the federal debt, this one, Burr-Hatch-Upton, is the only one of the eight plans that offers a clear path to accomplish it.

Introducing Real World Consequences Into The Health Reform Debate

Republican Congressional leaders, candidates, and think tanks have been consistent and candid about their preference and determination to repeal all or most of the ACA. Yet many ACA provisions have become established parts of America’s health system, including

- insurance exchanges;

- premium and cost sharing subsidies;

- coverage for young adults up to age 26;

- elimination of pre-existing condition exclusions;

- elimination of lifetime and annual benefit caps;

- Medicaid expansion;

- closing the Medicare prescription drug coverage gap called the “doughnut hole”;

- accountable care organizations;

- approval of biosimilar biopharmaceuticals;

and more. Public discussion concerning ACA repeal proceeds without consideration of the real and significant policy impacts and consequences. Public conversation needs to better educate Americans about the many significant policy impacts that would be wrought by repeal of the ACA.

Authors’ Note

The authors thank Kelsey Brykman and Ellen Fugate for their research support.